Market Pulse - 19 July 2021

Stocks sink on virus concerns

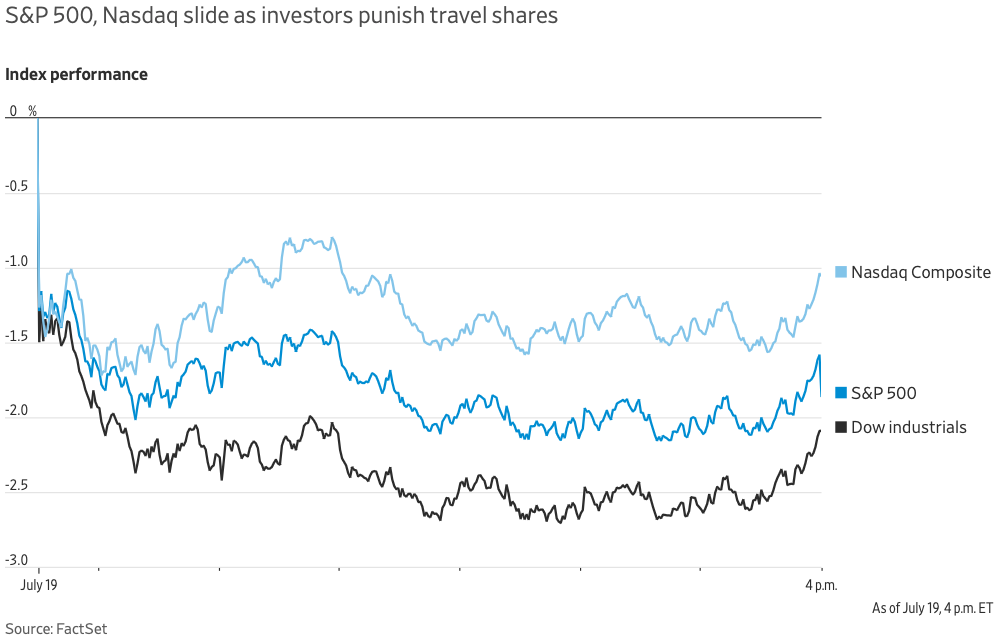

US stocks fell aggressively Monday on concern a rebound in Covid-19 cases would slow global economic growth. The selling picked up as the session continued and the Dow Jones Industrial average was currently headed for its biggest drop of the year.

The Dow dropped 724 points, or 2.09%, exceeding a 2% decline seen in late January. The S&P 500 fell 1.58% with energy, travel, and industrial sectors as the worst performers. The Nasdaq Composite lost 1.06%. Monday’s losses marked an acceleration after U.S. stock indexes dropped last week, snapping a three-week winning streak. The Dow was down over 900 points at its lowest level of the trading day.

The 10-year US Treasury yield continued to defy analyst predictions and fell to a new five-month low of 1.19%, further exacerbating fears about the slowing economy. Crude oil dropped over 5% to $68.62 a barrel on an OPEC agreement to boost production, concerns over a slowdown in demand as fall and winter seasons approach, and as Europe tinkers with the idea of Covid shutdowns again.

Stocks heavily tied to the reopening of global economies have been declining over the past few weeks as the spread of the Delta variant intensifies. The sell-off in airlines, cruise lines, industrials, energy, and financials all exacerbated their sell-off on Monday. However, we strongly believe that any Covid-19 related corrections in the market should be viewed as buying opportunities and investors with medium to long-term investing horizons should buy these dips in these sectors of the market. Investors should be patient when putting new money to work in equity markets as the remaining weeks of the summer will likely be a period of volatility and likely see a correction of approximately 10%.

The trend also raises questions about international travel. International and business travel have been largely missing from airlines’ recent rebound in bookings to pre-pandemic levels, though executives earlier this month said they have started to recover. However, the US still bars most non-US citizens from entering the country from the EU, UK, India, and other nations. The travel industry has repeatedly pressed the Biden administration to lift some of those restrictions, however with the uptick in Covid-19 cases, this doesn’t seem likely to occur until new daily cases begin to decline. There have also been reports in many US states of up to 18 week delays for Americans looking to renew their passports. This unexpected headwind will also have a negative impact on international travel.

Monday’s sell-off also began to trickle over into mega-cap technology, a sign that the recent internal rolling correction in speculative assets such as crypto-currency and travel related stocks is broadening out to overall equity markets. Facebook, Amazon, Apple, Microsoft, and Google were all red on the day after consecutive weeks of all-time highs and resilient outperformance in the market. Investors have fled to high quality companies with strong earnings and balance sheets as the Delta variant has dominated headlines recently. We believe that investors will find solace in high quality companies with strong earnings throughout the second half of the year.

The massive wild card in the market however is still the debate of whether inflation is transitory or not. The Federal Reserve has not dared to deviate from their script that inflation is transitory. We believe however that inflation will be high for longer than the Fed is predicting. Everywhere you look, the global supply chain is a mess with huge backlogs on everything from semiconductors, materials, automobiles, furniture, household appliances, etc. These delays in the supply chain have caused massive spikes in prices to transport these goods but have been passed on to the consumer as well. We believe that the supply chain will correct itself as the global economy fully opens and in turn this portion of inflation will be transitory, however we are starting to see wage inflation as there has been a shortage of workers and employers are forced to incentivize these individuals to come back to work with higher pay packages. Price inflation can be combated, however once wage inflation hits the economy, this is never reversed.

Our view is that we will not see a period of stagflation and out of control inflation like we did in the 1970s, but inflation will be higher for longer than the Fed is telling the market. This will be the most significant headwind in the market for the foreseeable future. We also believe that there is still tremendous upside in the economy for the second half of the year as many employers force their employees back into the office and cities. Consumer spending should broaden out and reach more areas of the economy especially the ones that have suffered the most throughout the pandemic.

We believe this current market sell-off will end in approximately a 10% correction. The market has not seen a correction of 5% or greater since October of 2020 and typically sees two 5-10% corrections every year. Volatility is completely normal in equity markets and especially as the US economy enters the mid-phase of the business cycle. We also believe as we come to the end of the year, interest rates will be meaningfully higher and approach 2% on the 10-year treasury as people realize the economy is going to make a big recovery. Investors should remain disciplined to their investment horizons and review their financial plans regularly as inflation could have a larger effect on achieving their financial goals than we have been used to.

Thank you for your interest.

If you would like to discuss the above or review your accounts, please feel free to set up a call by clicking here.